The grocery landscape: what marketers and media network operators need to know

Despite the rise of delivery services, the brick-and-mortar grocery store remains an integral part of the American consumer’s life. As such, grocery stores provide a uniquely impactful environment for advertisers to reach and connect with consumers effectively.

For brand marketers, the physical grocery store represents a critical last-mile touchpoint. It’s the moment of truth where purchase decisions are made.

For grocery retail media network (GRMN) operators, that same store is a media property: a place-based network with measurable audiences, verified shopper data, and scalable inventory across thousands of screens, shelves, and digital touchpoints.

New research unlocks actionable findings

The challenge, and the opportunity, lies in understanding who those shoppers are, how they behave, and where they are most receptive to messaging.

The People Platform’s research on grocery shoppers—which surveyed over 1,000 U.S. consumers across a pool of brands operating nearly 21,000 stores—delivers exactly that intelligence.

The data reveals clear, actionable consumer patterns that have direct implications for both marketing strategy and media network monetization.

Why the physical store still reigns

Before examining shopper behavior, it's worth establishing the scale of the opportunity. Despite growing digital adoption, 91.5% of all food and beverage purchases still occur inside physical stores. Yet in-store retail media remains one of the most under-monetized channels in the entire advertising ecosystem.

That gap is closing, and fast. In-store digital media experienced 47% growth in 2025, driven by the deployment of display screens in aisles, checkout lanes, and endcaps.

According to eMarketer, in-store digital formats are expected to drive 33% of all anticipated retail media revenue growth — trailing only on-site sponsored search and product placements.

Now, let’s dive into the data and see how some of The People Platform’s findings can help drive impact both for GRMN operators and marketers in this space.

Self-checkout adoption trends and demographics

Self-checkout usage in grocery stores is no longer a fad, but a go-to preference for many. More than half (52.6%) of all shoppers used self-checkout during their most recent trip.

Self-checkout screens represent one of the most captive and measurable placements in the store. Shoppers are stationary, task-focused, and present for a predictable duration. That’s a media operator's ideal audience condition.

- The demographic split: Adoption is highest among those aged 35–44 at 64.3% and those aged 18–24 at 60.0%.

- The drop-off: Preference for self-checkout remains high until the age of 55, where usage falls to 45.0% and eventually 38.8% for those 65 and older.

To continue to grow adoption, retailers must balance the speed and efficiency of automated lanes with the personalized service older demographics still clearly crave. This could include things like human assistance at the self-checkout lane or AI-enabled features that make the experience more intuitive.

For GRMN operators: Self-checkout screens are premium placement inventory. Their closed, dwell-time-rich environment warrants premium CPMs and should be prioritized in network build-outs and advertiser pitches.

For marketers: Ads displayed at self-checkout have proven influence at the final moment of decision. These placements are ideal for brand reinforcement, loyalty program prompts, and last-minute upsell messaging.

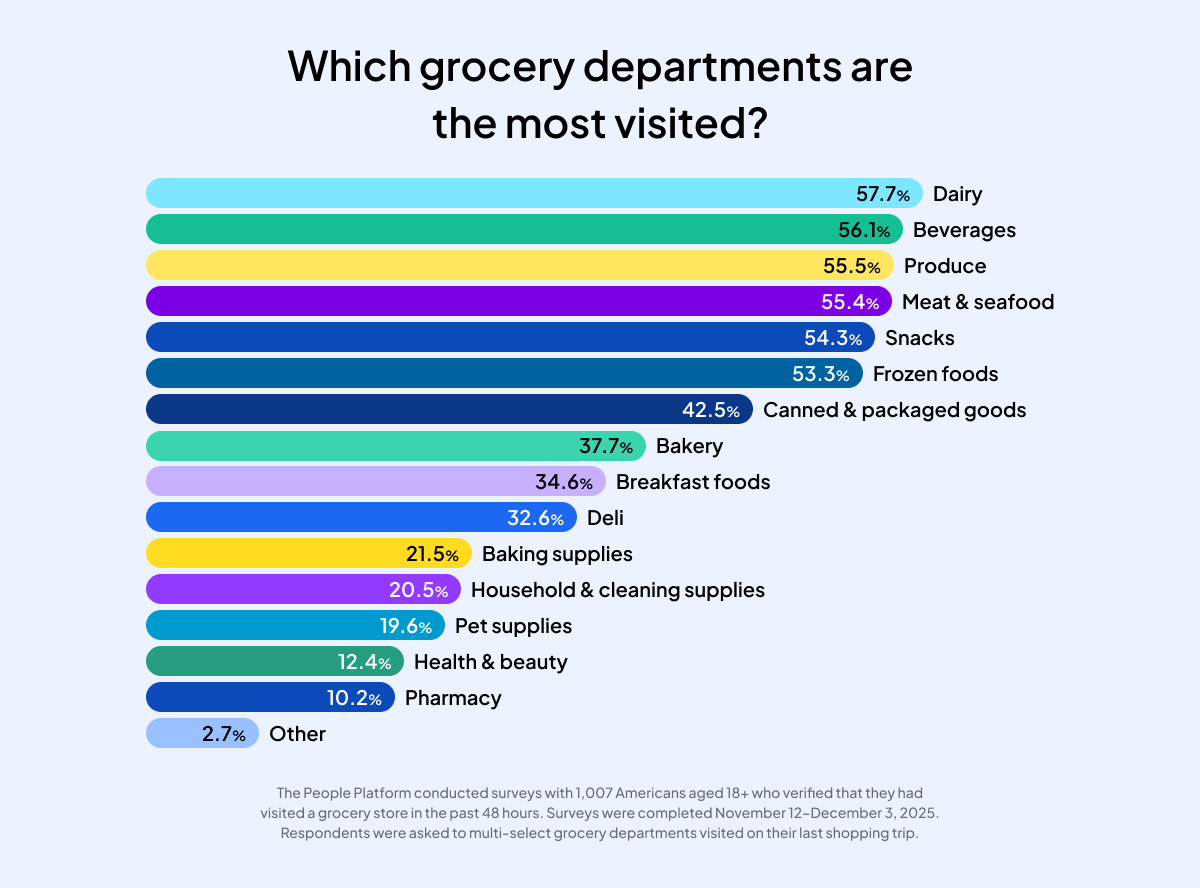

Power departments: maximizing in-store real estate

Shoppers are increasingly efficient. The average grocery trip length for the majority of shoppers (52%) falls between 15 and 44 minutes. Consumer movements during these windows remain remarkably consistent:

- Top destination: The Dairy aisle is the most frequented department in the grocery store.

- Perimeter shopping: More than half of all respondents visited Dairy, Beverages, Produce, Meat & Seafood, Snacks, and Frozen Foods during their most recent trip.

For GRMN operators: The Power Department perimeter is your network's premium inventory. Screens and digital placements in Dairy, Produce, and Beverages command the highest impressions per hour and should be packaged as flagship placements for CPG advertisers. Context-aware, AI-driven content that adapts by time-of-day or day-of-week can further amplify performance.

For marketers: Securing secondary placement or signage within the Dairy or Produce aisles is the most reliable strategy for exposing shoppers to products outside their pre-planned list. These environments are ideal for discovery-oriented, upper-funnel brand messaging.

The rise of high-value digital coupon clippers

While digital coupon usage in grocery stores currently sits at 39.7% of all respondents, this segment represents a massive opportunity for revenue growth.

The data shows a clear correlation: digital coupon users spend more, averaging a basket size of $154.00, which is roughly 20% more than the general average basket size of $129.40.

This research underscores specific trends around digital coupon adoption:

- Peak usage: Shoppers aged 35–44 are the most engaged with digital coupon technology, with 52.4% using them.

- Adoption trends: Usage of digital coupons is 39.0% among those aged 55–64, dropping to its lowest point of 33.0% for shoppers aged 65 and older.

- Explaining a dip: Interestingly, the 45–54 age demographic has a lower digital coupon adoption rate (36.5%) than their elders in the 55–64 cohort. One possible reason: The 45–54 demographic is likely in the midst of juggling kids and careers, leading them to prioritize getting the shopping over quickly (without spending extra time hunting for digital deals).

For GRMN operators: Digital coupon behavior is a measurable signal of high-intent, high-value shoppers. Networks that can tie coupon redemption data to screen exposure — particularly in high-traffic zones like Dairy or Produce — can offer brands a compelling closed-loop attribution story.

For marketers: Simplifying the coupon experience within store apps, especially for users aged 45+, is a direct lever for basket size growth. Personalized, push-based offers (rather than opt-in searches) can close the adoption gap without requiring behavioral change.

Grocery shopper loyalty, frequency, and store switching

Overall, the study's resondents visited a grocery store with some amount of frequency—with the 55–64 age group returning to a store the most (57.2% of that demographic reported 4+ visits in the past four weeks).

But are they patronizing the same retailer, or spreading their spending among multiple ones? While two-thirds of respondents hold loyalty club memberships, the data on multi-store grocery shopping behavior suggests that "loyalty" does not mean "exclusivity."

- High frequency: Loyalty members shop an average of 4.8 times per month.

- Store hopping: Even with this regular frequency, 71% of shoppers reported also going to a different grocery store in the past four weeks. These respondents averaged 3.3 trips to other locations during that time.

The implication is clear: loyalty programs drive frequency, but not exclusivity. Shoppers are not monogamous.

For GRMN operators: This multi-store behavior is actually a media network opportunity. Shoppers who are comparison-minded and deal-driven are highly responsive to in-store media. Networks that can demonstrate share-of-wallet capture, not just visit frequency, will command stronger advertiser investment.

For marketers: Loyalty rewards should be engineered around spend thresholds rather than visit counts. Mechanics like "spend $20 more this trip to unlock a reward" are designed to capture a larger share of a shopper's total monthly grocery budget, not just their presence in the store.

Tapping the vital power spender profile

The research highlights the 35–44 age bracket as a critical "power spender" category— and arguably the most valuable audience profile for any grocery media network to activate.

- This demographic maintains one of the highest average grocery basket sizes, at $164.

- Beyond high spending, 35–44-year-olds are the most digitally engaged, boasting the highest usage of digital coupons at 52.4%.

- They are also the heaviest adopters of self-checkout technology, with 64.3% utilizing automated lanes.

This demographic doesn't just spend more — they are more reachable through digital channels, more responsive to personalized offers, and more likely to interact with the very technologies that make GRMN measurement possible. They represent the ideal intersection of high spend, digital fluency, and behavioral predictability.

At the same time, the 55+ segment — with digital coupon usage between 33% and 39% — represents a significant growth opportunity. These shoppers have the time and inclination to engage with deals; they simply need more intuitive tools and in-store prompts to activate that behavior.

For GRMN operators: The 35–44 cohort should anchor your network's audience story when going to market with CPG brands. Build audience segments around verified behavioral data — basket size, coupon redemption, department visits — not just demographics. This is what separates a grocery media network from a traditional OOH buy.

For marketers: Tailor loyalty reward structures and digital ad creative to the 35–44 group's behavior patterns: personalized, convenience-forward, and reward-driven. For the 55+ segment, invest in simplified in-store digital experiences and screen-based prompts that reduce friction around digital offer discovery.

The evolution of grocery retail media networks (GRMNs)

The behavioral data above doesn't just inform marketing strategy — it defines the commercial architecture of the modern Grocery Retail Media Network.

In 2025, GRMNs matured into full-funnel commerce media engines, integrating first-party shopper data, loyalty insights, and closed-loop measurement to tie digital ad exposures directly to in-store sales. The results are drawing significant investment:

- Total spend on grocery-specific retail media networks (RMNs) surpassed $8.5 billion by early 2025, maintaining a double-digit growth trajectory as grocers leverage high-frequency loyalty data.

- The in-store digital media segment grew by 47% in 2025—officially becoming the fastest-growing format in the retail media ecosystem, far outpacing traditional on-site web display.

- 92% of consumer goods advertisers now rank retail media as their "most important" marketing channel, prioritizing it over legacy search and social platforms due to its closed-loop measurement capabilities.

- As of late 2024, 70% of grocery retailers had finalized plans to deploy or scale in-store retail media technology—such as smart carts and digital endcaps—within an 18-month window.

- Global retail media ad spend is projected to exceed $184 billion in 2025 (surpassing total TV ad spend) and is expected to grow at a 10.4% CAGR through 2029.

For GRMN operators, the competitive pressure is real: Amazon Ads holds approximately 75.2% of the U.S. retail media market, with Walmart Connect at 8.1%, according to Emarketer data.

But the grocery channel holds a structural advantage that neither Amazon nor Walmart can fully replicate: the verified, high-frequency, in-person shopper visit.

Every trip to the store is a measurable media event — and our data shows those events happen nearly five times per month among loyalty members.

The winning GRMN strategy

Based on our research, there are 5 key points to consider for a grocery store media network that wants to fully capitalize on brick-and-mortar consumer audiences.

- First-party data activation: Use loyalty, coupon, and basket data to build verified audience segments

- In-store screen networks: Prioritize “Power Department” placements with high dwell time and frequency

- Programmatic and contextual delivery: Integrate AI-driven content that responds to time of day, foot traffic, and shopper demographics

- Closed-loop measurement: Connect ad exposure to incremental sales, not just impressions

- Off-site extension: Amplify in-store audiences across CTV, mobile, and social to deliver full-funnel reach

How The People Platform's audience measurements can help drive insights

- Learn more about The People Platform and explore our audience measurement solutions designed for media network owners and operators.

- Follow us on LinkedIn to stay up to date with the latest trends and information for Grocery Retail Media Network operators and marketers.

- Don't forget to also explore the broader suite from The Marketing Cloud to unlock AI-driven marketing solutions that help teams across market research, comms, creative, and media.

Research methodology for this study

The 2025 grocery shopper study used a blended methodology including mobility data, online panels, and social media targeting. TPP conducted surveys with 1,007 people aged 18 or older who verified they had been to a grocery store in the past 48 hours to understand grocery shopping behavior in 2025. Surveys were completed from November 12 to December 3, 2025. The study focused on brands with at least 100 stores, including Aldi, Publix Super Markets, Kroger, Save-A-Lot, and Food Lion.